Asking for a cash donation may seem easier than a Major Gift, but is it the right thing to do for your organization?

When you ask for cash donations you really don’t need to put the time into helping your donors while they are trying to help you and your organization.

When you ask for cash you don’t need to put the time into becoming a competent advisor or one who is willing to spend time with donors and provide direction or connections to those who can assist the donors in making a wise donation decision.

When you ask for a cash donation you don’t really need to learn new things like asset based giving or options for giving.

When you ask for cash you’re not building the sustainability of your organization but meeting your current needs. But asking for assets makes sense for your donor and for your organization.

When you ask for a cash donation you are asking your donor to give out of the smallest bucket that they have in the overall assets. Cash is an asset but so are stocks, mutual funds, real estate, art, tangible personal property and registered investments and even private business shares.

I am willing to bet that the cash holding for most of your donors is truly the smallest bucket of assets of all of their holdings.

Then why do you keep on taking the easy way out?

If you invested in the stock market over the past year, the gain represents an opportunity to discuss the advantages of donating shares to your charity rather than donating cash. The share donation is pre-tax thus eliminating the tax owed on the donated shares. Rather than donating cash where you’ve already paid the tax, your donation actually cost you more than if you donated the equivalent amount in shares.

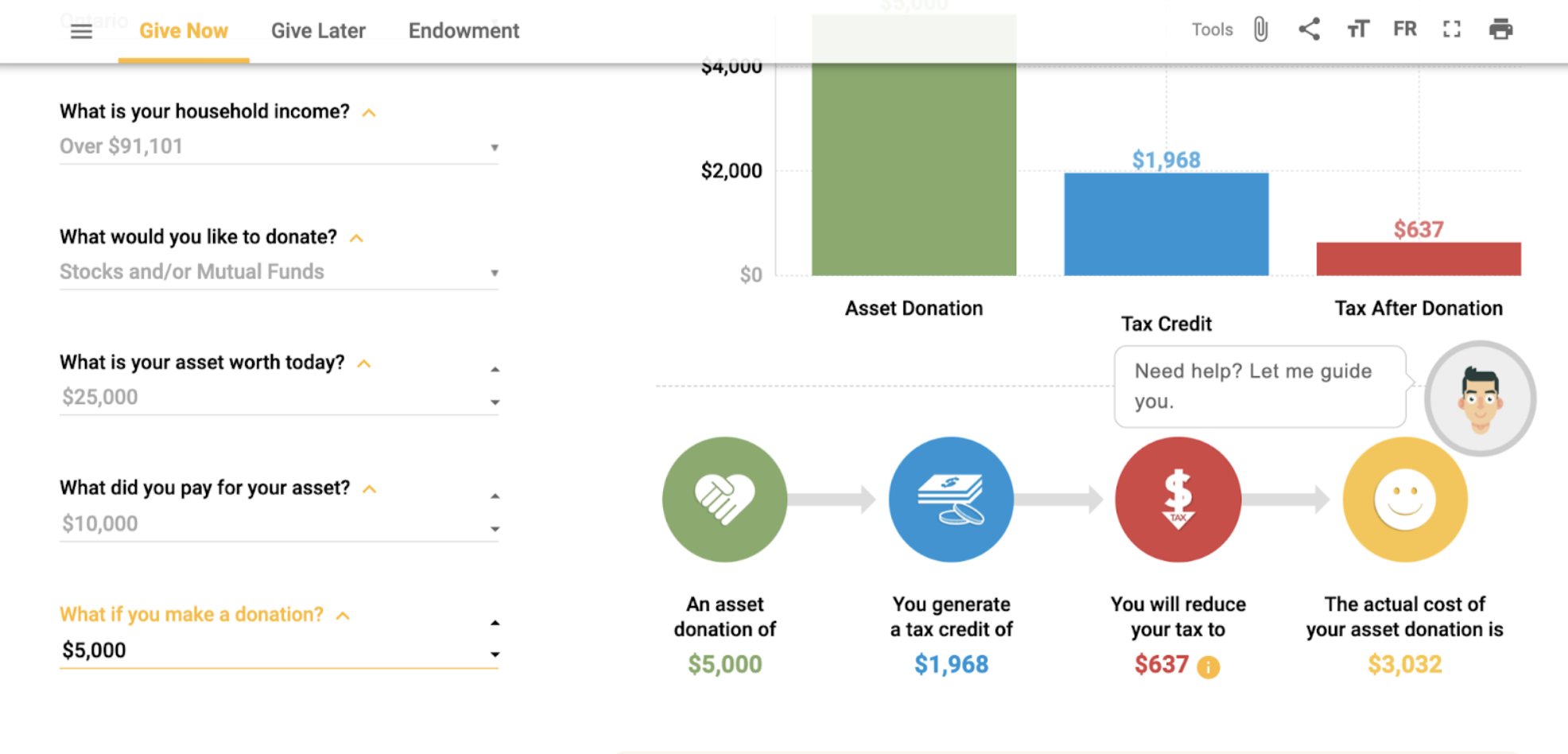

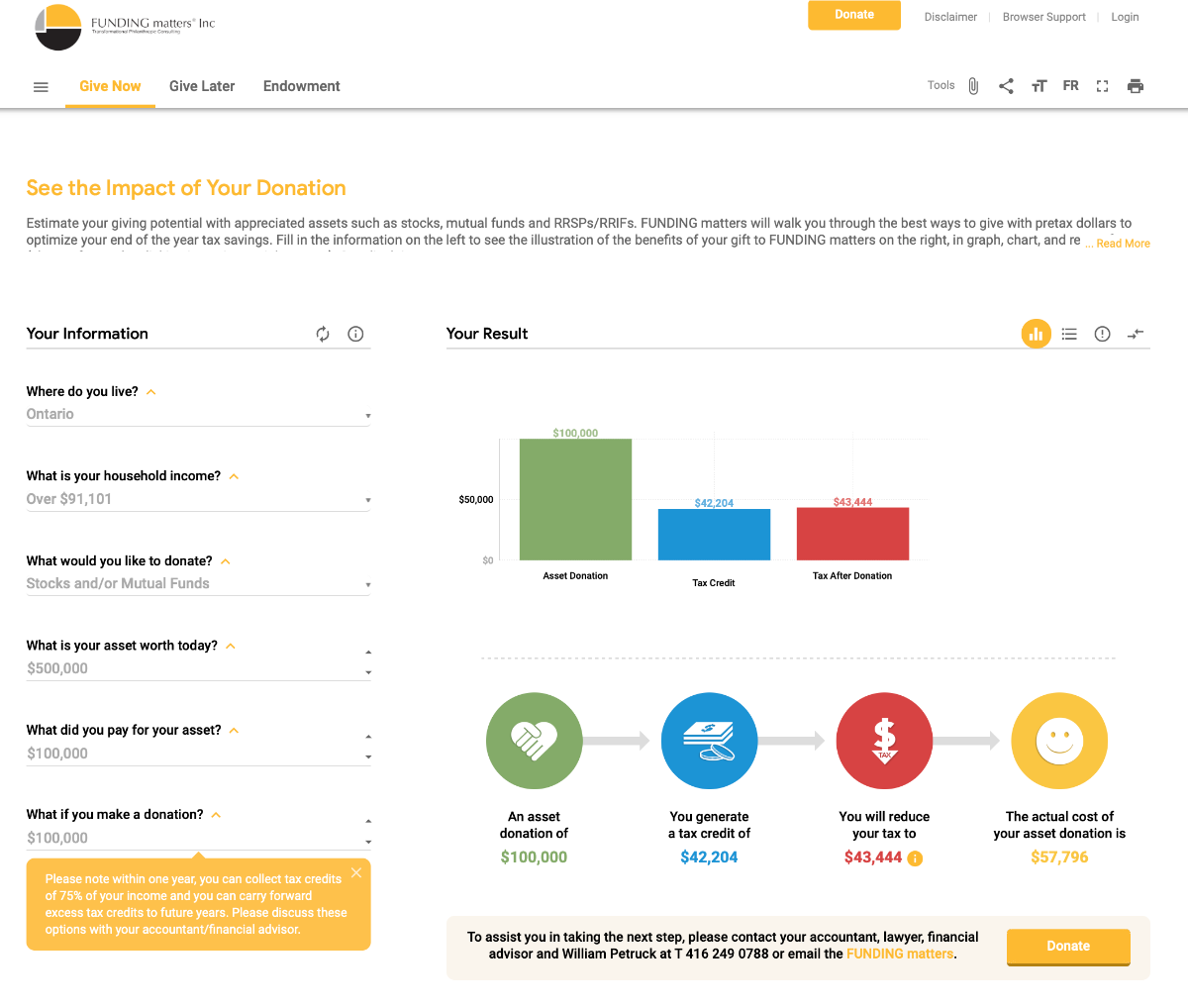

In the Giftabulator scenario above, the donor lives in Ontario and has a household income of $91,101 which determines their tax bracket. Their shares are worth $25,000 and they paid $10,000 for them. Not a bad return on investment. The tax on the asset is $2,605. A Major Gift of $5,000 provides a tax credit of $1,968 and reducing the tax to $637. The actual cost of their donation when transferred from their investment account to the charity is $3,032.

Invest in yourself, invest in your organization, embrace new approaches to donor engagement, donor education and organizational sustainability.

For more information, please feel free to contact me.

In our last blog, Gary expressed that the amount of real estate in existence was finite, and he didn’t want his donation to fall into the black hole. He was satisfied with the establishment of the organization’s foundation which would be a golden goose for the charity. So, he decided that part of his estate would include two significant real estate holdings to the organization.

He had discussions with his accountants who took great lengths to ensure that these assets could be received and realized by the organizations. Ultimately, this took months of ongoing discussions for Gary’s wishes to be fulfilled. Although he passed away, Gary was at peace knowing that his land was being used by a good cause.

Yet, while Gary went this route, it wasn’t the only direction available to him. You see, not all giving is straightforward, and there are many strategies that we explored with Gary as he was evaluating his options. Gary could have created a Donor Advised Fund (DAF) had he not chosen to donate to a charity directly. Let’s explore what this option would have looked like.

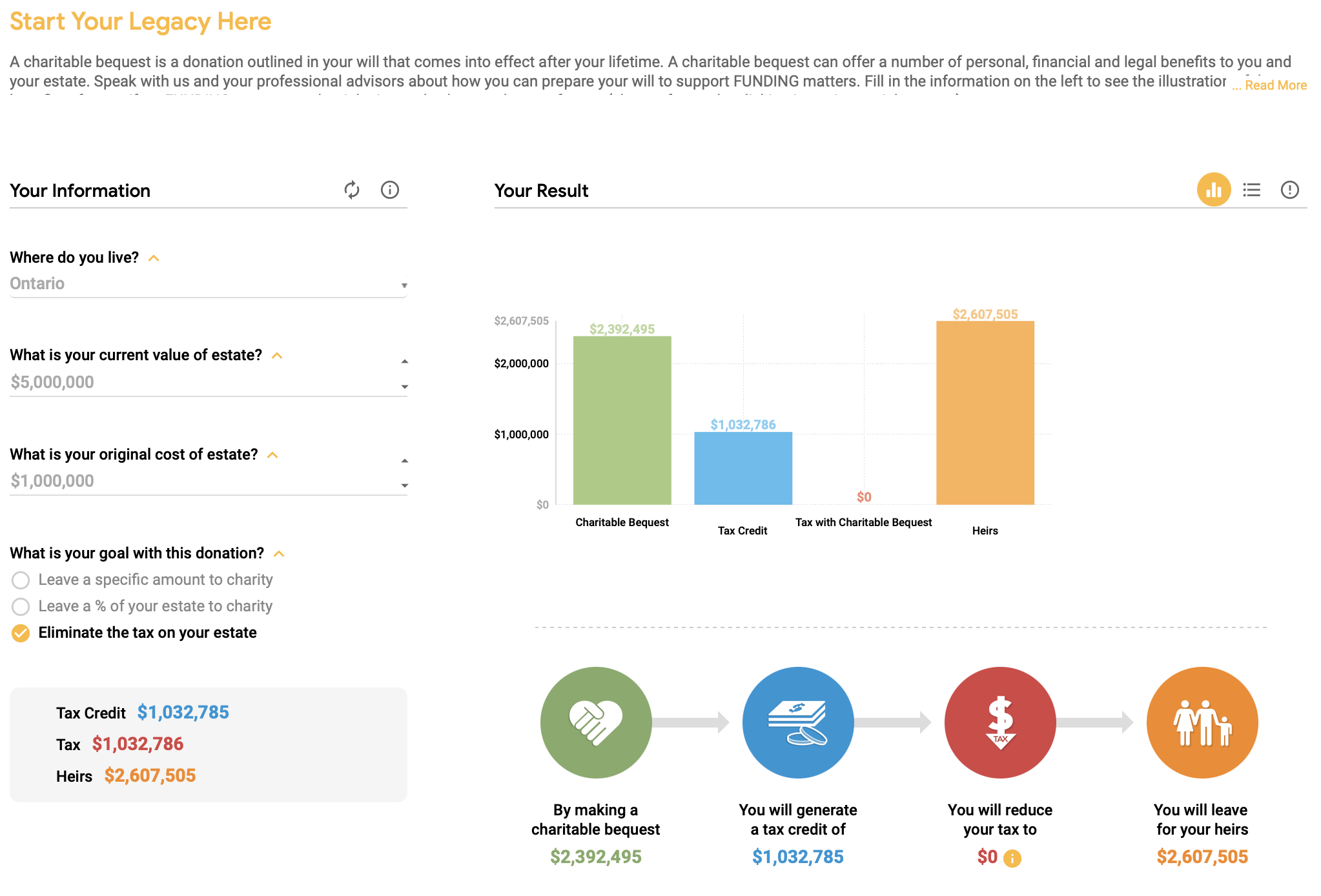

Above) Gary’s donation resulted in him eliminating the tax through his charitable contribution. Gary’s heirs received $2,607,505 and Gay’s charity received $2,392,495. It’s was a win-win-win for all!

What is a Donor-Advised Fund?

A DAF is a giving account established at a public charity. It allows a donor to…

Make a charitable contribution

Receive an immediate tax deduction

Recommend grants from the fund over time

One of the best parts is that donors can contribute to the fund as frequently as they’d like, and they can also recommend grants to their favorite charitable organization whenever it makes sense for them.

DAFs are surging in popularity for philanthropic Canadians because of increased awareness. More than ever, advisors are discussing giving options with their clients. One 2018 survey of financial advisors showed that 91 percent believed that discussing philanthropy with clients was “important,” while 53 percent of those individuals saw it as “very important.”

When you use DAFs, donors receive an immediate tax deduction for their contribution, and they have similar tax benefits as a private foundation. Bonus? You don’t have to deal with administrative responsibilities.

How Can I Get Started with a Donor-Advised Fund?

Contribute assets

Establish your DAF by making an irrevocable contribution of your personal assets. This could be in the form of stock, real estate, cash, etc.

Receive your tax deduction

Once you’ve established the DAF, you’ll be eligible to claim an itemized tax deduction for charitable contributions. The amount of the deduction will ultimately depend on several factors, but this is one of the primary benefits of giving through this means.

Personalize your account

DAFs can be structured in a way that helps you meet your goals. You’ll be able to name your fund whatever you like, appoint individuals to help you manage the responsibilities, design a legacy plan, etc.

Invest your assets for growth

The assets in your DAF are recommended based on your recommended strategy. Plus, any investment growth is tax-free!

Support your favorite charitable organizations

Once you’ve established your donor-advised fund, you can start recommending grants to the charitable organizations that mean the most to you.

Final thoughts

Ultimately, Gary decided that he wanted to make a difference for others but not get too complicated with other strategies. If you’re in his position be sure to explore all the planned giving strategies available to you. Visit FUNDING matters for more information.

I am pleased to be part of the organizing committee Session 4 presenter and sponsor for Knowledge Hub.

Every not-for-profit organization needs to hear stories and insights about how organizational leaders have navigated their organizations through this period and how they are planning in moving forward.

For the past few weeks, we’ve been reviewing the nine potential ways that you can give to charitable organizations. So far, we’ve reviewed stocks, registered retirement investments, and small business shares. This week, we’re diving into real estate with a unique donor named Gary.

Gary’s Story: Donating Real Estate to Charity

Gary wasn’t your average donor. He said two things that reveal who he is and how he thinks. “Land — they’re not making more of it!” and “I don’t want to pay taxes when I die.”

These two sentiments aren’t often heard together in a donor discussion, but as a retired contractor who had invested in land development over the years, Gary focused on people, places and things. He was a widower with one adult child, and he was a hard-working individual who could always be counted on to financially support his favourite organizations.

For instance, one of Gary’s charities once received a $1 million challenge grant. Without hesitation, he pledged $100,000. His philanthropic giving was always done quietly and without recognition. When he saw the community’s donations were at $850,000, Gary called to kick in that last $150,000. Of course, everyone wanted to know, “Who was the final donor?” The response was “Anonymous.”

But Gary wasn’t done with his giving. As he described, he had large tax obligations due to his large amount of taxable capital gains. His accountant alerted him to update his will and told him to plan to allocate his assets and look at which organizations might help him reduce his taxes.

At FUNDING matters, we’re familiar with how this can be done thanks to the Power Donor Experience and the GIFTABULATOR. If you’re in a similar situation to Gary, make sure you check out our resources to minimize your taxes.

Gary would often say that he felt that he was putting his money into a “black hole” when donating to charities. He never knew where the money went or how it was spent. No one in his family shared his spirit of community support or charitable giving either.

However, thanks to his accountant’s advice, Gary knew that charitable giving could help him out of his dilemma of paying taxes when he died. To get this process started, Gary approached a charitable organization about establishing a foundation. When Gary passed, the organization would receive a donation from Gary.

The process ended up working out well for him. The foundation was established, the board was nominated and elected, the Investment Policy Statement (IPS) was created, and information about the new foundation was slowly shared. The IPS was based primarily on stocks, mutual funds, and cash donations from estates.

While Gary was alive, he had a $3 million property that he acquired many years ago. With real estate values at an all-time high, this would have been an ideal time to sell; however, it also would have meant immense capital gains tax. Fortunately, he also had the option to donate the property.

The property was donated, and the charity’s foundation received the largest donation in its history. Gary requested that the organization retained the property until he passed since it could be used as a wonderful retreat for community members. It could even generate new revenue for the charity!

Final thoughts

Gary has since passed, but he gave direction in his estate for another major asset to be given to the foundation he created. In the next blog, we’ll cover Gary’s estate bequest.

Main Street: The Backbone of the Economy and Charitable Organizations

In the last blog, Sophie’s Legacy, we discussed how Registered Retirement Investments can transform estate planning. As soon as potential donors have access to the FUNDING matters Power Donor Experience (PDX) and the GIFTABUALTOR, their calculus can change.

Simply put, most people don’t know how to make tax-efficient donations. When they have the proper tools to understand how to do this, they’re much more willing to donate to the charitable organizations that need their help. Today, we’ll talk about small business shares, and how a man named Joe made a $1million donation to his favourite charity and still found a way to benefit his family.

How Donating Capital Assets Can Benefit Everyone

As of December 2017, the Canadian economy totaled 1.2 million employer businesses. Of these, 97.9 percent were small businesses, 1.9 percent were medium-sized businesses, and 0.2 percent were large businesses. More than half of Canada’s small businesses are concentrated in Ontario and Quebec (440,306 and 249,685 respectively).

According to Trevor R. Parry M.A. LL. B LL.M (Tax) CLU TEP, an Ontario lawyer focusing on tax, most of the taxes are paid by small business owners, and they should be able to direct their taxable capital gains to benefit their communities — not only in taxes but also in charitable giving. Trevor suggests, the gift of shares could be both a living tax plan and a testamentary one. In the first case, the business owner would gift shares of the company to a charity.

As the entrepreneur owns those shares personally, the gift will result in creating a Charitable Donation Tax Credit which is particularly useful as they are likely exposed to some top-rate taxation (53.53% in Ontario).

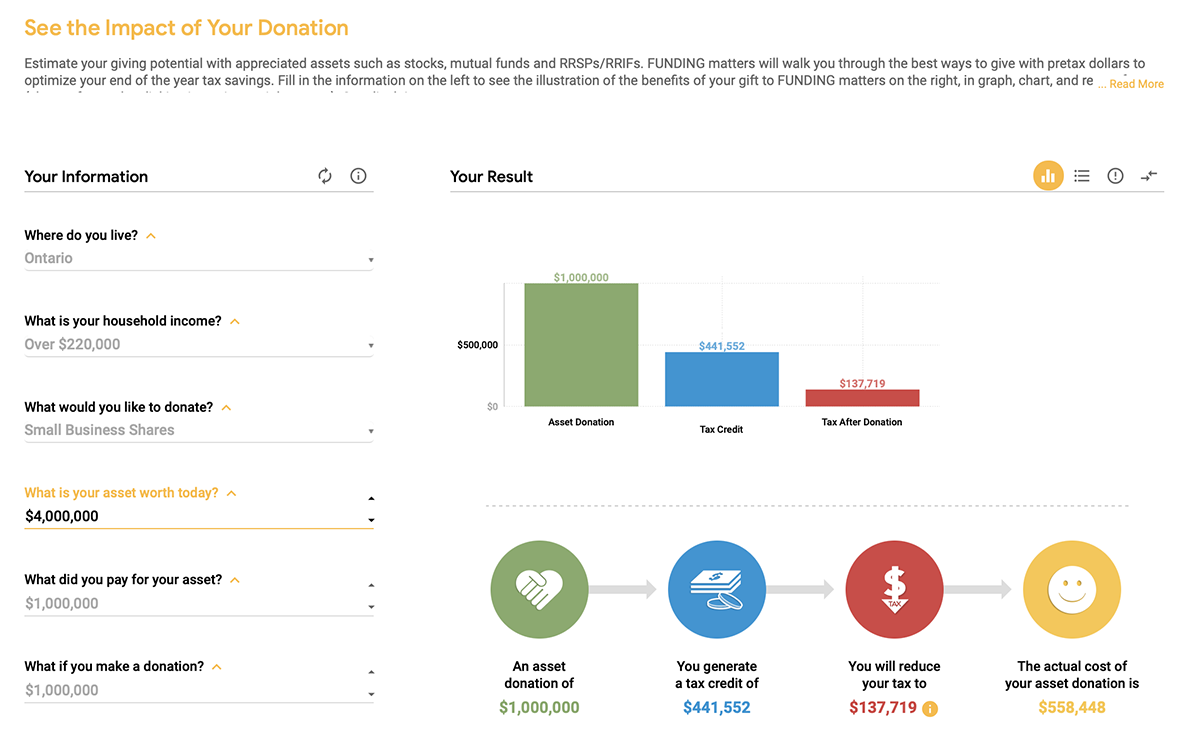

Joe’s Story

In Joe’s case, he and his advisor decided that it was the right time to make a significant donation to his favourite university. How much was that donation? $1,000,000.

Here’s a screenshot of the GIFTABULATOR with the information about his $1,000,000 donation plugged in.

As you can see, his asset is not only worth 4 times as much today, but he also generated a significant tax credit and reduced his tax to only $137,719. In the end, he made a $1,000,000 donation while only paying $558,448.

Final thoughts

Overall, the success of the economy and charitable organizations is based on the backbone of small businesses. With the guidance of financial advisors, prospective donors can wisely create tax-efficient lasting legacies for the communities that they serve.

In last week’s blog, From Spare Change to Real Change, we talked about major and planned giving through stocks. At FUNDING matters, our goal is to help your organization allow donors to visualize the various types of assets that can be used to make a donation. In this week’s blog, we’ll be discussing charitable giving through Registered Retirement Investments. To start, let me take you back to a conversation I once had with a woman named Sophie.

Sophie’s Legacy

Back in 2008, I was advising for a non-profit home for the aged on their capital campaign. The project was an expansion and modernization of a long-term care home, and we hosted a series of donor discussions and presentations (PDX Step 4: Communication) on the topic. I specifically enjoyed teaming up with advisors that had an association with the organization (PDX Step 5: Leverage and Alliances). The presentations were initially titled “Leaving Your Legacy.” The early presentations drew a small number of attendees. It was only after following up with those who made time to attend and seeking their feedback that they greatly appreciated the tax, legal, and estate planning information acquired from the session. They knew they were getting valuable information.

As a group, we thought that the insight was helpful and wanted to continue to offer this type of advice, but instead of focusing on legacy, we pivoted and renamed the sessions “Estate Planning for You and Your Family.” Immediately, we noticed a significant increase in the turnout. By altering the focus, the session now allowed us to address the options for giving as part of both financial and estate planning. Tax-efficient major gifts and planned gifts were both woven seamlessly into the presentations.

Sophie, an elderly lady diagnosed with terminal cancer, attended all of the estate planning sessions. She would bring piles of estate planning literature from various financial institutions that she collected. She was on a mission to get educated and have meaningful discussions with her advisors.

When I ran through different scenarios using the GIFTABULATOR in the presentations, she was able to visualize various potential scenarios. Did she want to make a donation, a bequest, or both? Sophie pulled me aside, and I met with both her and her advisors over the next few months. We walked through different scenarios that may make sense for her. Sophie wanted to know how much she might pay in tax on Registered Retirement Investments.

So, I plugged in some examples both in the GIFTABULATOR Give Now (Major Gift) and Give Later (Bequest), and I showed her the outcome from the hypothetical numbers.

Then she asked, “How much tax will I owe on a $12 million Registered Retirement Investment?”

I was initially taken aback. Was she serious? She said, “Put in the numbers. I don’t want to pay taxes. I would rather see my money put to use for those organizations that are doing important work. I want to make a difference. I am a widow, and my children and grandchildren are taken care of. There will be enough for them if I donate.”

Today, Sophie’s legacy lives on at universities, libraries, and homes for the aged. All of these spaces were important throughout different stages of her life, and she had the opportunity to demonstrate her commitment to them even after she passed.

How Visualization Made the Difference for Sophie

Before our presentations, Sophie hadn’t considered a Registered Retirement Investment. She couldn’t conceive of what it would be or visualize herself doing it. She didn’t know the various types of assets that could be used to make a donation. Once she did, she was ready to do it.

Having the ability to plug in the numbers and see what it looked like helped make it real for her. The GIFTABULATOR is the tool that every organization needs for major and planned gifts. Easy to understand, use, and explain, it’s a tool that forecasts the potential for giving (and for a zero-tax bill!)

See the below screenshots and how Sophie’s estate and legacy were structured.

From Spare Change to Real Change: Enlightened Philanthropy and How to Achieve It For All

In the previous blog, Why Visualization is the Key to Success, we talked about the importance of visualization to help donors, their families, and their advisors construct major and or planned gifts. This blog will continue the conversation, specifically focusing on how this visualization method pertains to stocks.

Here’s what you should know.

Option 1: Stocks and Mutual Funds

As briefly discussed in our last blog, the GIFTABULATOR is the best tool to use when helping illustrate estate, financial and philanthropic planning. It helps you minimize taxes while making the world a better place through planned or major gifts.

And — believe it or not — cash is not always king in the world of philanthropy. While many donors choose to donate using cash, it isn’t always the right move. What often happens is that donors will sell stocks in order to give a tax donation. Unfortunately, selling appreciated assets leaves the donor with the responsibility of paying capital gains tax.

Instead, they could select to gift their stocks to their charity of choice. This gives the donor a tax reduction and helps them avoid paying a capital gains tax in the process. Additionally, depending on the size and type of their gift, it could also lead to a reduction in their taxable estate.

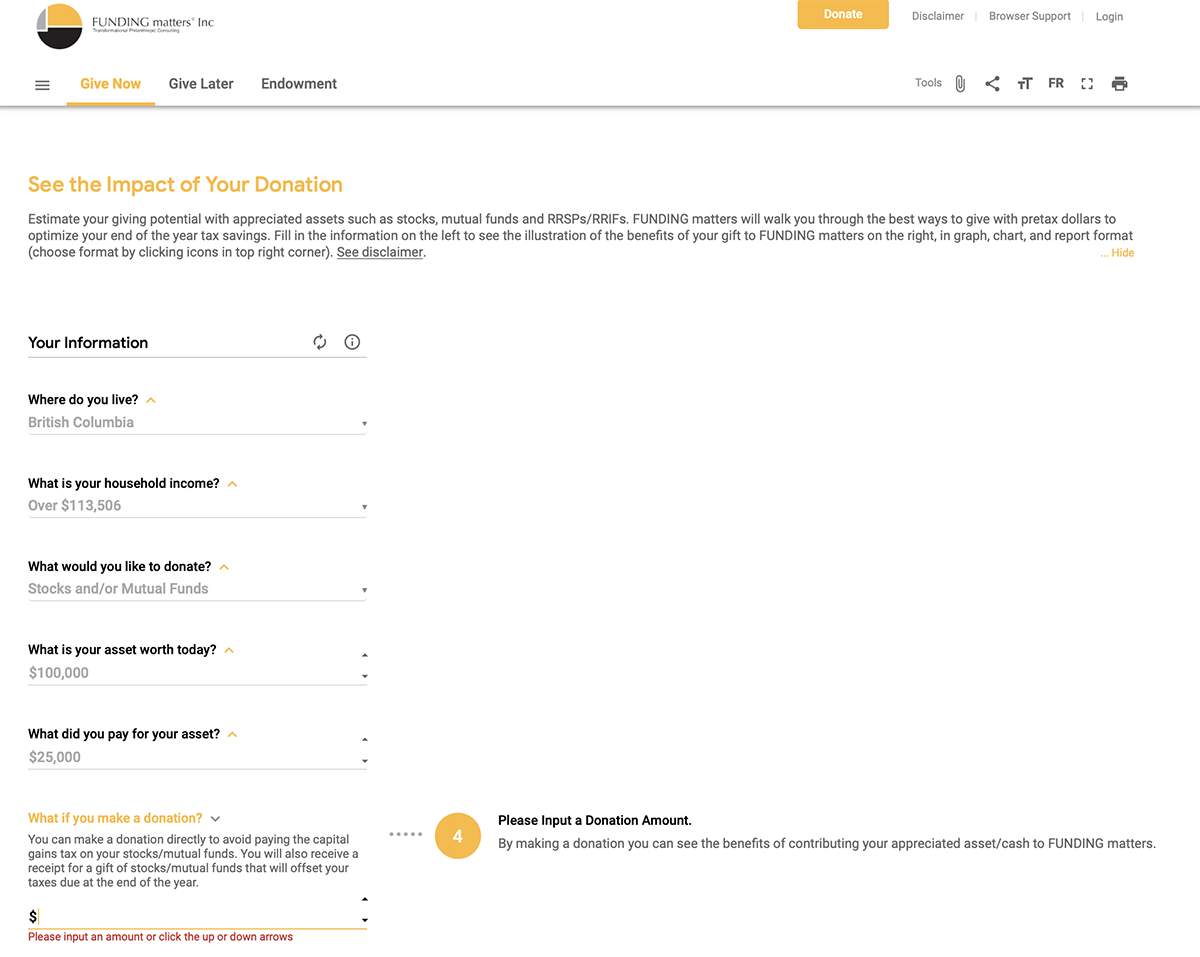

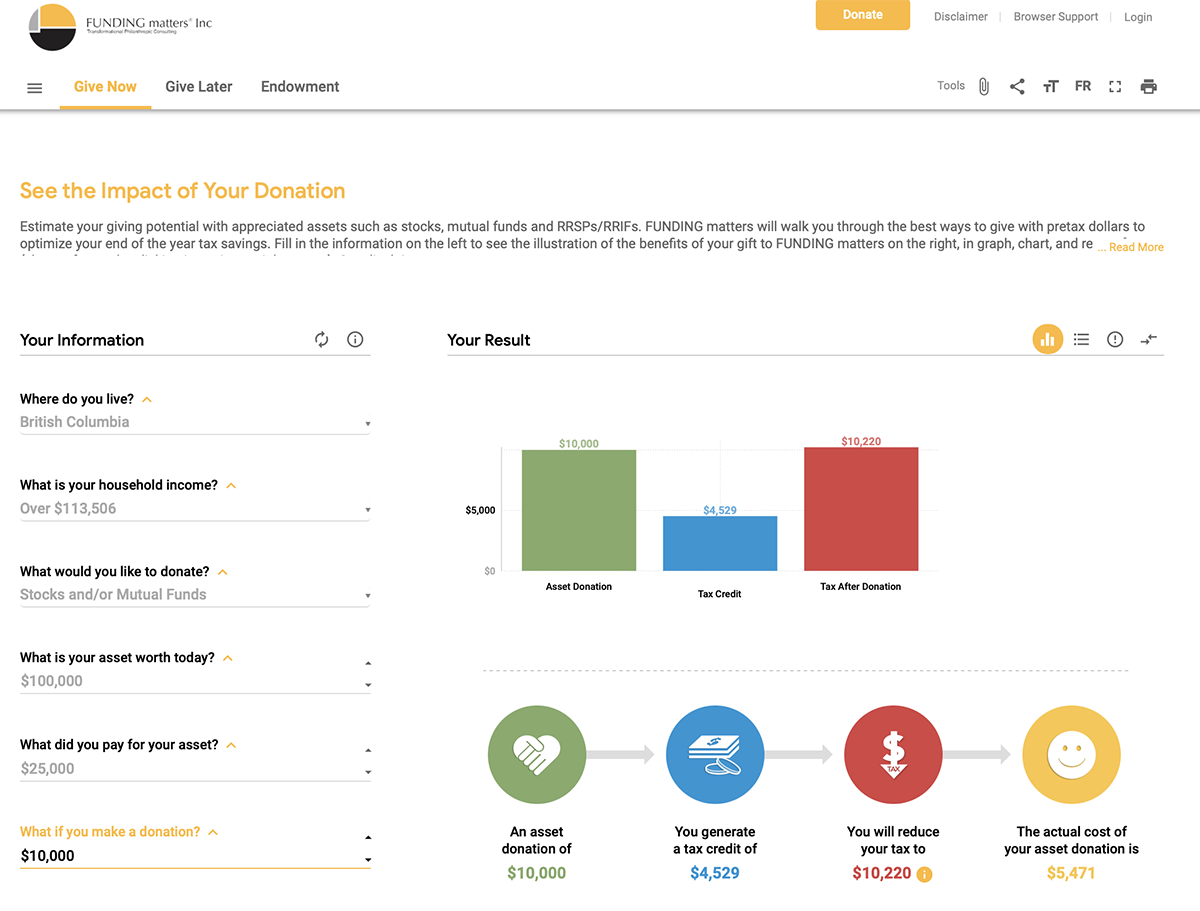

Calculating a Tax-Efficient donation is really easy when it can be visualized. First select the Province you live in. Let’s select British Columbia for our example.

Then you’ll be prompted to select an asset. For this blog select Stock. You will see that the current value of the asset is $100,000. Feel free to change the asset to any amount.

Giftabulator will then have the amount that you paid for your asset that is now worth $100,000. Populated into the app is amount suggesting you paid $25,000. You have a taxable capital gain of $75,000. $100,000 – $25,000. That math was simple. Now with the information you have input Giftabulator will calculate how much tax you owe on your capital gain if sold.

By inputting a donation amount of $10,000 you will see on the coloured charts your $10,000 donation which is illustrated in green. As well, you will see your tax credit from your $10,000 donation of $4,529 in blue. The red chart represents the tax you will owe from your $75,000 taxable capital gain. With your $10,000 donation your taxable capital gain has been reduced from $14,749 to $10,220. Finally, the actual cost of your $10,000 donation is illustrated in gold as $5,471.

Including Every Donor in the Conversation

Recently, we came across the article Making the Most of Mid-Level Donors. The authors, Sarah DiJulio and Yoonhyung Lee, state, “Mid-level donors are often overlooked at non-profits, even though they are among the most generous and loyal supporters and may have the potential to give much more if they are treated well. How can your organization attract, keep, and inspire mid-level donors to give more?”

The reality is that these mid-level donors are the backbone of your organization’s annual funding. The issue is how to convert many of these donors into major gift and planned giving donors. The key is to provide the tools that can illustrate the benefits associated with a larger donation and indicate where the funding can be sourced. Since most donors give from the “wallet” in the form of a credit card, cheque or cash, the ideal major gift should be sourced from appreciated assets with a taxable capital gain.

Why is this important for your donors to know? Illustrating a donation from an appreciated asset with a taxable gain will help the donor understand the benefit associated with a donation on which they will be paying tax if not used partially or wholly as a charitable gift. After all, no one wants to pay tax, and you’re providing them a fulfilling alternative through a donation to your organization!

Final thoughts

Over the next several weeks, we’ll be discussing all of the ways that potential donors can give to your organization. In fact, so many may not know that the money that they have in stocks can become a charitable gift. That “spare change” they have lying around can create real change — especially if you include every donor in the conversation!

Why Visualization is Key to Major and Planned Giving Success

In the past several blogs, we’ve covered five of the seven steps of FUNDING matters, Power Donor Experience (PDX). The goal of the PDX is to help individuals and organizations visualize how they need to manage the relationships and develop a prospect pipeline. Underlying all of the steps is the ability to visualize that donation at the end of the tunnel.

In this Harvard Business Review article, Scott Berinato argues that there are four different types of visualization, but all are just a means to an end. “Visualization is merely a process. What we actually do when we make a good chart is get at some truth and move people to feel it—to see what couldn’t be seen before. To change minds. To cause action.”

This blog will focus on why visualization is the key to success as you continue to engage donors and how you can help them visualize their future contributions.

How Visualization Can Help You The PDX lays out several visualization steps for you – perhaps you just didn’t know that’s what they were until right now. The most prominent are Step 1 and Step 4.

Step 1 (Brainstorming and Strategy) is perhaps the greatest opportunity for visualization. Berniato references brainstorming directly as a key tool in idea generation. Whiteboards, butcher paper, the back of a napkin, or a Google Doc – however you brainstorm best is up to you, but this type of visualization is seen as a way that business can work and answer complex challenges. For you, it’s how you will ensure planned giving success. You’re laying the foundation and beginning the process of identifying, cultivating, and soliciting high-net-worth donors.

Step 4 (Communication) is also a highly-valuable step in the visualization process. This is when you have the opportunity to prepare communication materials to build your prospects’ enthusiasm and commitment. This is what Berniato calls “idea illustration.” He says the focus should be on “clear communication, structure, and the logic of the ideas.” By creating these materials, you’re able to visualize the optimal outcome (a donation), and your donors are able to visualize donating themselves.

How To Help Donors Visualize Helping donors visualize is also essential to achieving major and planned giving. As noted above, you directly help this process along in Step 4 of the PDX by providing written materials, but what if there was an even better way? Say you have a donor who lives in Ontario and their household income is in the range of $95,000 and $115,000. This range indicates their tax bracket on income. They have been contributing $1,000 to your organization each year in December as part of their year-end tax planning. They support your mission as both a donor and a volunteer, and you feel secure in their commitment to your organization.

Now, you want to show them a simple illustration of another method of tax-efficient giving that they may do at any point in the year. Ideally, this would be triggered by growth in an asset like a publicly-traded stock or a mutual fund. If they purchased Shopify shares at $100 per share and today their shares are worth $1,500, their capital gain on their Shopify shares is $1,400. If sold, they would be required to pay the tax on the capital gains.

In helping your donor visualize how the part of all of the tax on their capital gain can be used to make their donation, it demystifies the donation process and allows them to visualize actually make that donation. In the end, this makes both you, your donor, and your organization happy.

Fortunately, you don’t have to sit with each and every prospect donor and lay out all of the different options. The GIFTABULATOR does this for you. Here what it will show donors:

How they can support your charity without impacting their lifestyle

How a donation to your charity can help them minimize their taxes and those of their beneficiaries

How they can ensure that their values and beliefs are reflected in their estate planning choices

How their potential to give back is based on their assets as opposed to their income

Final Thoughts

Visualization is key to major and planned giving success because it allows both you and your prospective donor to better understand how you can make it happen.

As Yogi Berra once said, “If you don’t know where you’re going, you’ll end up someplace else.”

For more information on the GIFTABULATOR, visit here. It’s easy to understand, use, and explain. It’s a tool individualized for each prospective donor that will demonstrate their potential giving capacity and help them visualize donating to you.

Physics in Fundraising: How to Use Leverage and Friends to Lift Heavy Objects

Physics is a science that deals with matter and energy and their interactions. Matter and energy are both required to successfully raise funds.

Fundraising is a never-ending race, and in order to maintain your speed, your organization must use leverage through your or your stakeholder’s efforts to engage prospects. Leverage builds on the interests, values, priorities, and intent of your donors.

Leverage can also mean taking something you’ve done previously and using it to its maximum potential or advantage to increase your results in the future, especially where your donor has demonstrated interest.

Just as we have addressed in the previous blogs (Step 4: Communications and Step 3: Connectors), having a series of conversations with your donors will uncover some of their “hot spots” for giving and their personal feelings toward your organization. Building a discussion around their values provides tremendous insights and can make a tremendous difference for both your donor and your organization.

To obtain major and planned gifts for your organization, FUNDING matters recommends using leverage and alliances in engaging prospects. In this blog, we’ll discuss how leverage helps prospects understand the benefits and impacts of major or planned gifts. Let’s get started.

What are the three steps to using leverage and alliances to cultivate prospects?

1. Understand the donor and their family’s interests, values, views, and priorities. The insights can be sought through brainstorming, research, and support provided by volunteers and/or stakeholders; or just having a conversation with the prospect.

2. Engage your network and connections in prospect engagement. This will help open doors that seemed impenetrable. Your stakeholders or friends can act as links to individuals that you weren’t sure how to connect with.

3. Introduce relevant estate, financial, and taxation planning. This type of planning with their families and advisors can make a tremendous difference and increase donations by generating a larger tax credit to reduce taxable capital gains.

Success in any fundraising initiative depends on your ability to connect your charity’s mission, goals, and objectives with the donor’s values, views, interests, and priorities. Research makes this connection. Your charity can find where the money is through prospect research (Step 2: Prospect ID and Research) either directly or indirectly. Let me explain further.

I can’t tell you how often I have been approached by a volunteer in an organization who offers a name of an individual that I should approach. The prospective donor was never on anyone’s list to approach for a donation, but there we are finding a way to reach out. The volunteer not only offered the name but also a willingness to facilitate the introduction. These hidden gems are only unearthed through alliances that are in many cases not obvious.

The second step in this process is utilizing the Leadership Committee’s relationships and connections in prospect engagement. Typically, FUNDING matters will invite prospects to use the Giftabulator Best Ways to Give web app at this stage. This allows prospects to explore the idea of giving a gift.

Developed by FUNDING matters Inc., the Giftabulator ”Best Ways to Give” illustrates how to structure major and planned gifts. Giftabulator Best Ways to Give allows individuals to privately run through multiple major and planned giving donation scenarios.

The Giftabulator optimizes the donations section of your client’s website to guide individuals through the process of formulating a gift that is tailored to their unique financial situation. They’ll ultimately come away with the knowledge that making a gift to your campaign is achievable.

Throughout this process, the Leadership Committee and prospects develop an alliance. While major and planned gifts from total strangers occur, they are exceedingly rare. Coordinating deeper relationships with prospects through genuine engagement helps to solicit major and planned gifts in the future. FUNDING matters can help facilitate the cultivation and solicitation process.

We understand the need to engage in discussions with family, financial and legal advisors, and accountants. We know that taking these steps can ensure a successful legacy, and we take great care in developing customized, compelling, and well-thought-out proposals that specifically address donors’ needs and expectations. These proposals also help to maximize our revenue.

Throughout the fundraising process, FUNDING matters provides its clients with the experience, judgment, and wisdom of our counsel. This third step pertains to the ability to discuss relevant estate, financial, and taxation planning with your prospect. It is highly important for the family of the prospect to feel comfortable with their donation when it comes to discussing philanthropy with prospective donors and their families.

Why does this approach work?

Relationships between organizations and prospects begin with knowledge and evolve through the stages of interest, investment, and finally, ownership. Cultivation helps accelerate the process and increase the likelihood of securing the maximum gift possible.

Unless there is a corresponding readiness to give, the capacity to give will not necessarily result in a proportionate gift. Establishing a relationship (alliance) between the organization and the prospect before asking for the gift provides additional leverage.

Finally, in addition to the on-going personal cultivation by the campaign leaders, it will be necessary to hold a series of meetings where prospective donors and leaders can learn more about the project. In most cases, these meetings will be one-on-one (Step 1: Virtual Brainstorming).

Final thoughts

In this blog, we talked about Step 5: Leverage, which helps to engage with prospects in a way that allows them to understand the impact of major or planned gifts. The never-ending race of fundraising is always more successful if you’re coordinated in your approach and prepared to demonstrate impact.

You can learn more about the GIFTABULATOR here and read more about the 7 Step Power Donor Solution here.