In-kind acts for the holidays

Gifting stocks, other investments excellent way to support charities this season, while helping to significantly cut your tax bill come spring

By: Joel Schlesinger

Most people dig a little deeper in their wallets this holiday season to help those in need. But some can also look to their portfolio by donating stocks, bonds and other investments that can have big impact on charities while reducing their own tax bill come spring filing their return.

In-kind donations refer to directly transferring ownership of shares of Apple Inc, for example, from a non-registered investment account (i.e. not a RRSP or TFSA) to a charity, which can then sell those shares and use the proceeds to fund its operations.

“If your stocks are doing incredibly well, it’s a great way to increase the amount of money you can donate to an organization while also increasing” the tax benefit you receive, says Amanda Leuschen, vice-president of strategic partnerships and philanthropy at United Way Winnipeg.

Of course, donating in-kind is not for everyone simply because not a lot of people have non-registered investment accounts.

But those who do hold stocks, bonds, mutual funds, exchange-traded funds, real estate and even shares in certain private corporations in a non-registered account may want to consider in-kind gifts.

“It’s often a win-win,” says Ana Plotnicoff, director of philanthropy at United Way.

The charity receives a substantial gift; the donor gets a tax receipt worth up to 75 per cent net income in a given year, and by transferring — rather than selling the shares first and giving the charity cash — capital gains tax does not apply.

“Instead of selling the securities and donating the cash, you’re much better off to donate the stocks directly because there is more of a beneficial tax impact to you,” says Lydia Potocnik, head of estate planning and philanthropic advisory services at BMO Private Wealth.

Already the non-refundable tax credits (provincial and federal combined) are generous for givers. Donors receive 25.8 per cent of their donation back in tax savings on their first $200 ($51.60) and then a combined credit for as much as 50.4 per cent for amounts exceeding $200 for the province’s highest income earners.

Founder and chief executive officer of Benefaction Canada Nicola Elkins says the federal government made in-kind donations attractive to givers when it changed the tax rules in 2008. The change eliminated taxes on gains in value on assets when directly transferred (in-kind) to a charity, or any other Canada Revenue Agency (CRA) certified donees. (Those include, by the way, journalism organizations, Canadian amateur athletic associations, arts service organizations and even the United Nations.)

“It has driven a lot of additional donations into the charitable sector,” Elkins says. “It’s increasingly popular for gifts of publicly traded securities and happens all the time, but this time of year is the busiest.”

For wealthier Manitobans and their advisors, none of this is news.

Toward the end of the year, they often pore over their portfolios to make in-kind gifts, fine-tuning the amount to maximize the benefit for the cause they want to support, and their taxes.

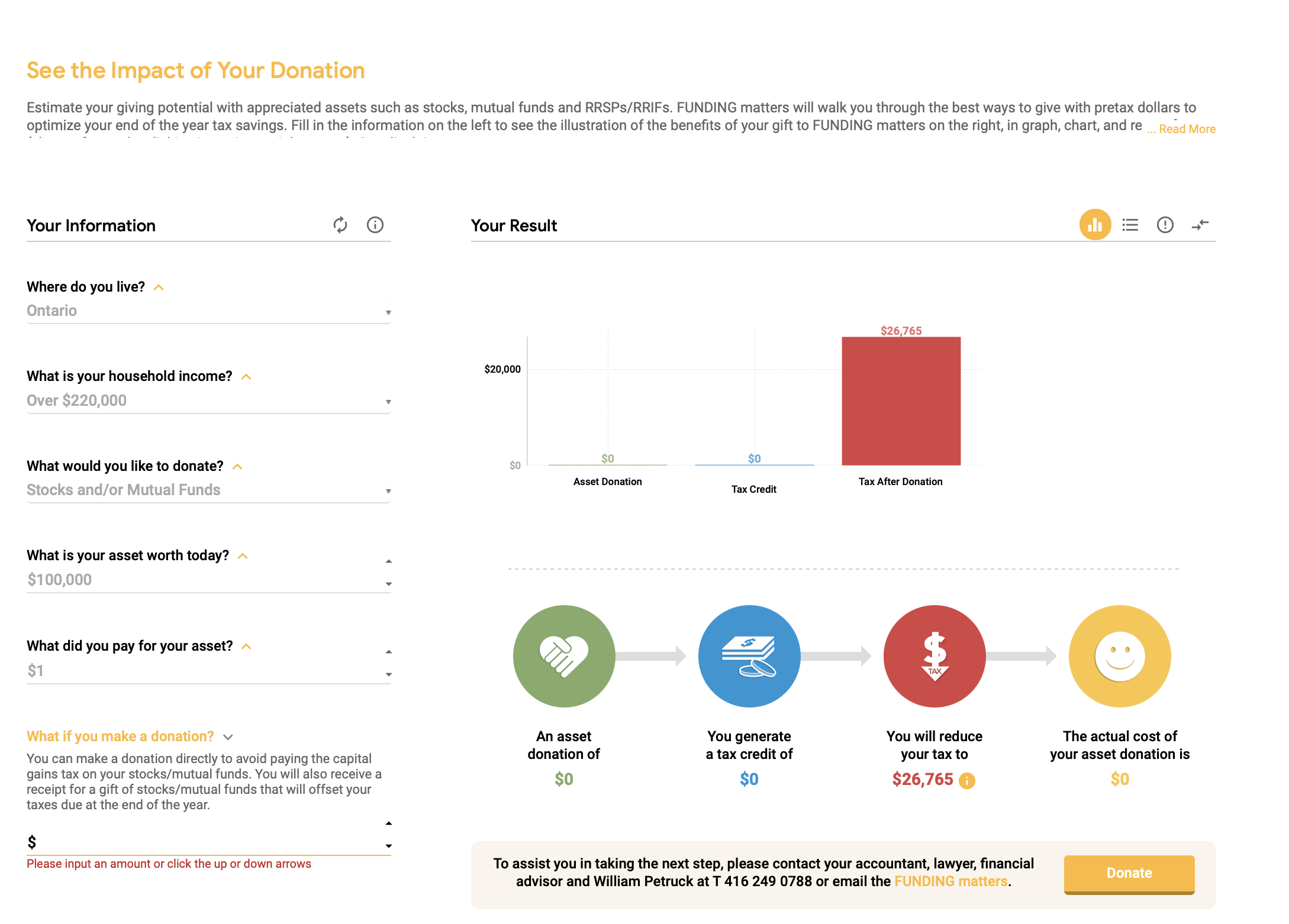

While not overly complicated, illustrations — or more aptly online calculators — help demonstrate the impact of a gift in both respects.

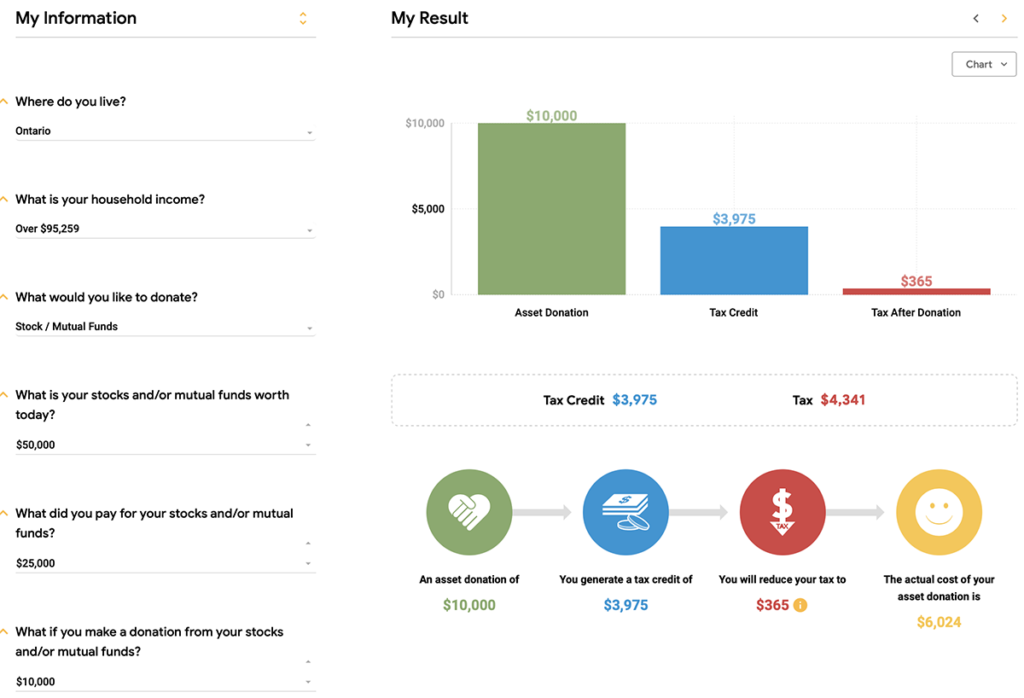

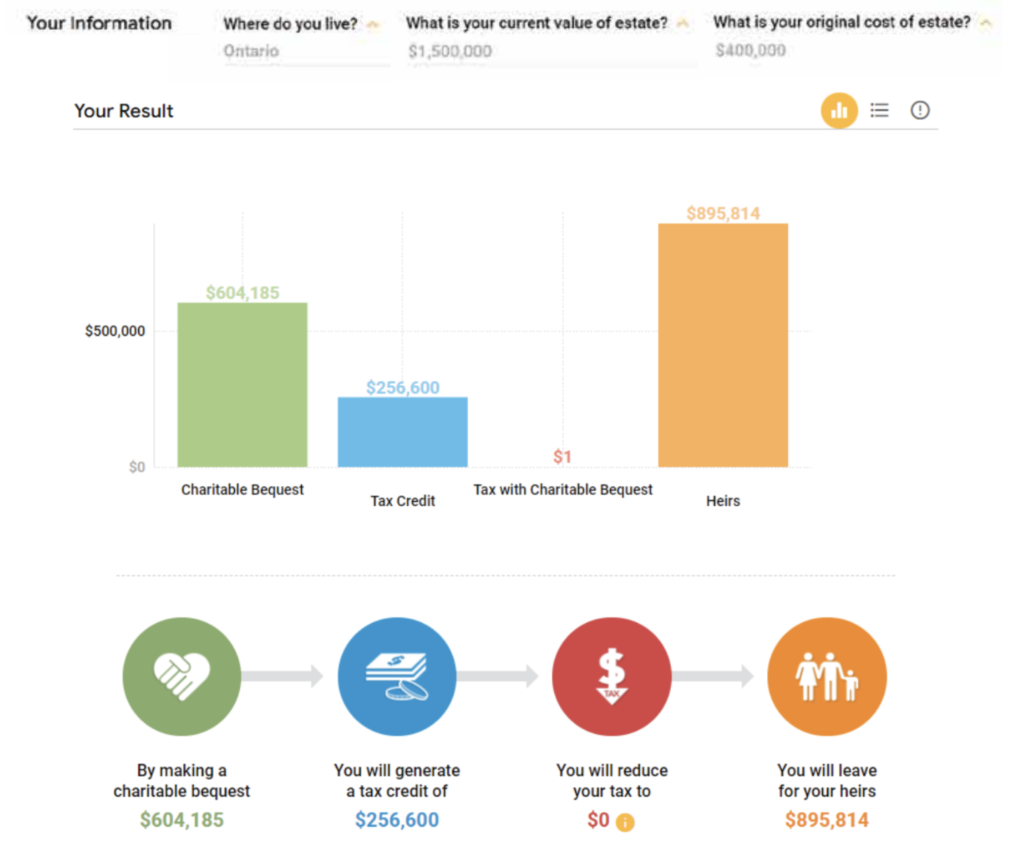

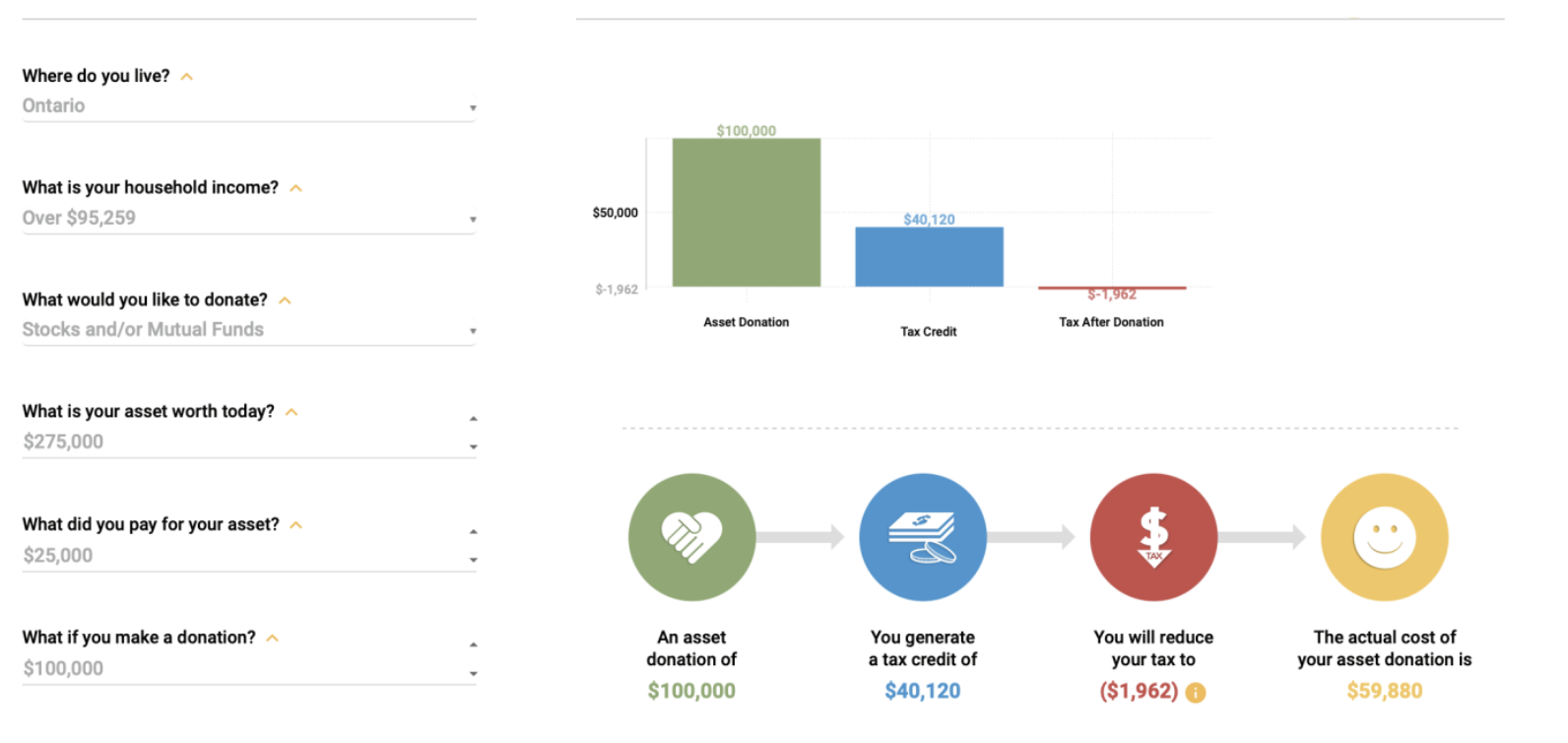

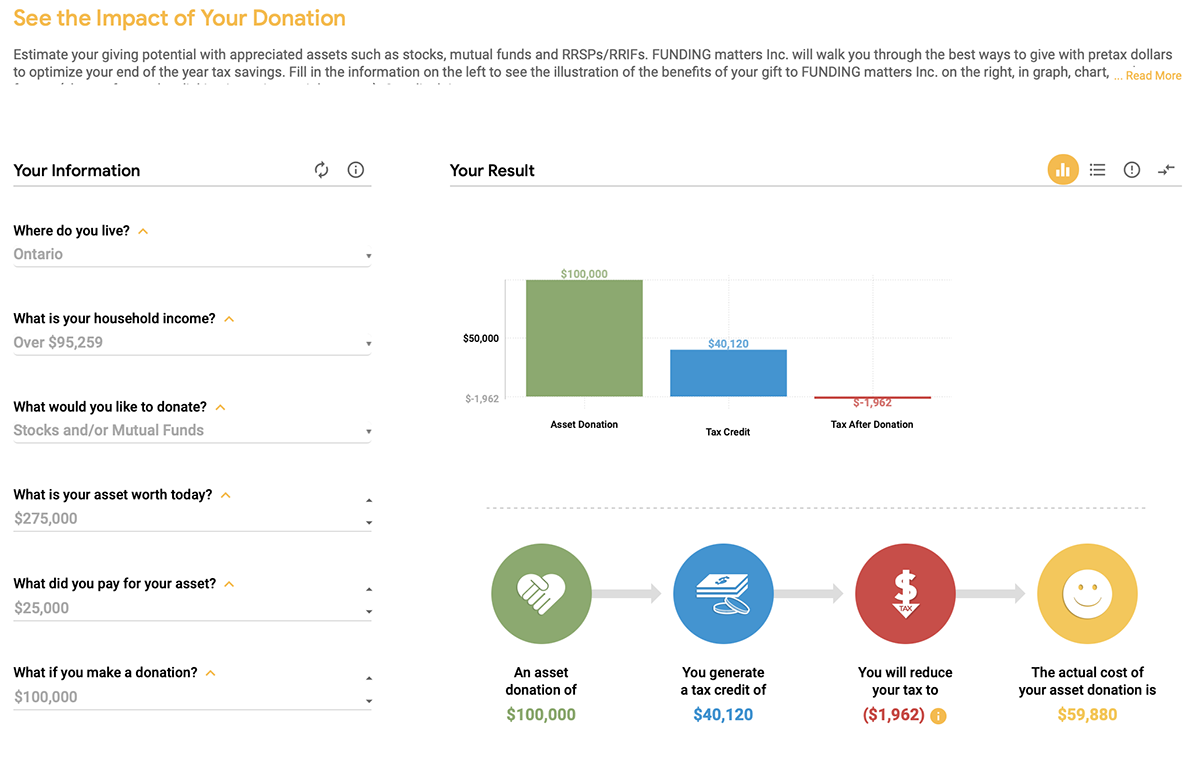

Those online calculators include the ‘GIFTABULATOR,’ mostly for advisors and charities to show their donors or clients the benefits of giving assets or cash.

“People are visual learners, and that’s why we created GIFTABULATOR — a learning tool where they can see the benefits,” says William Petruck, president and CEO of Funding Matters Inc. the organization behind the calculator.

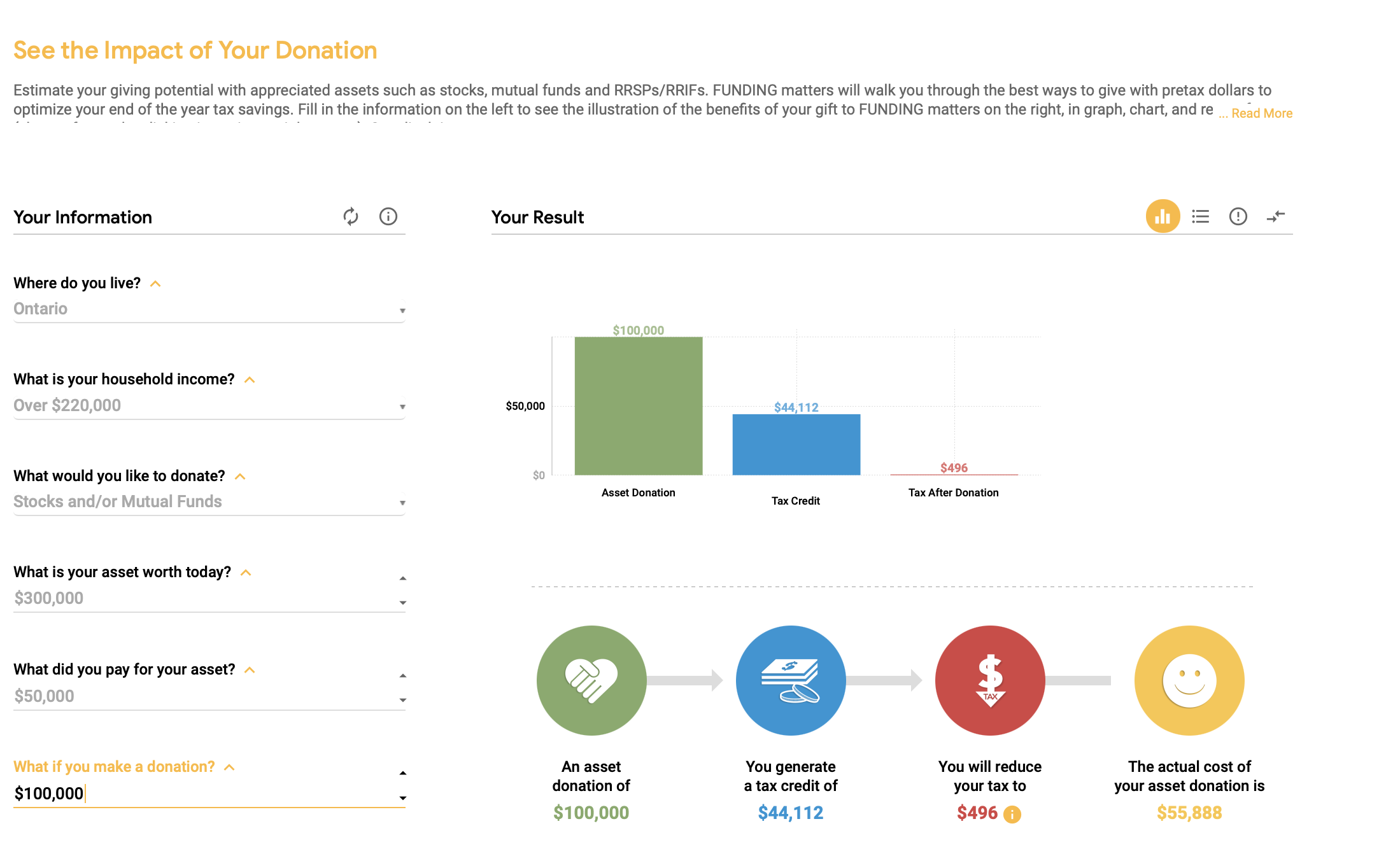

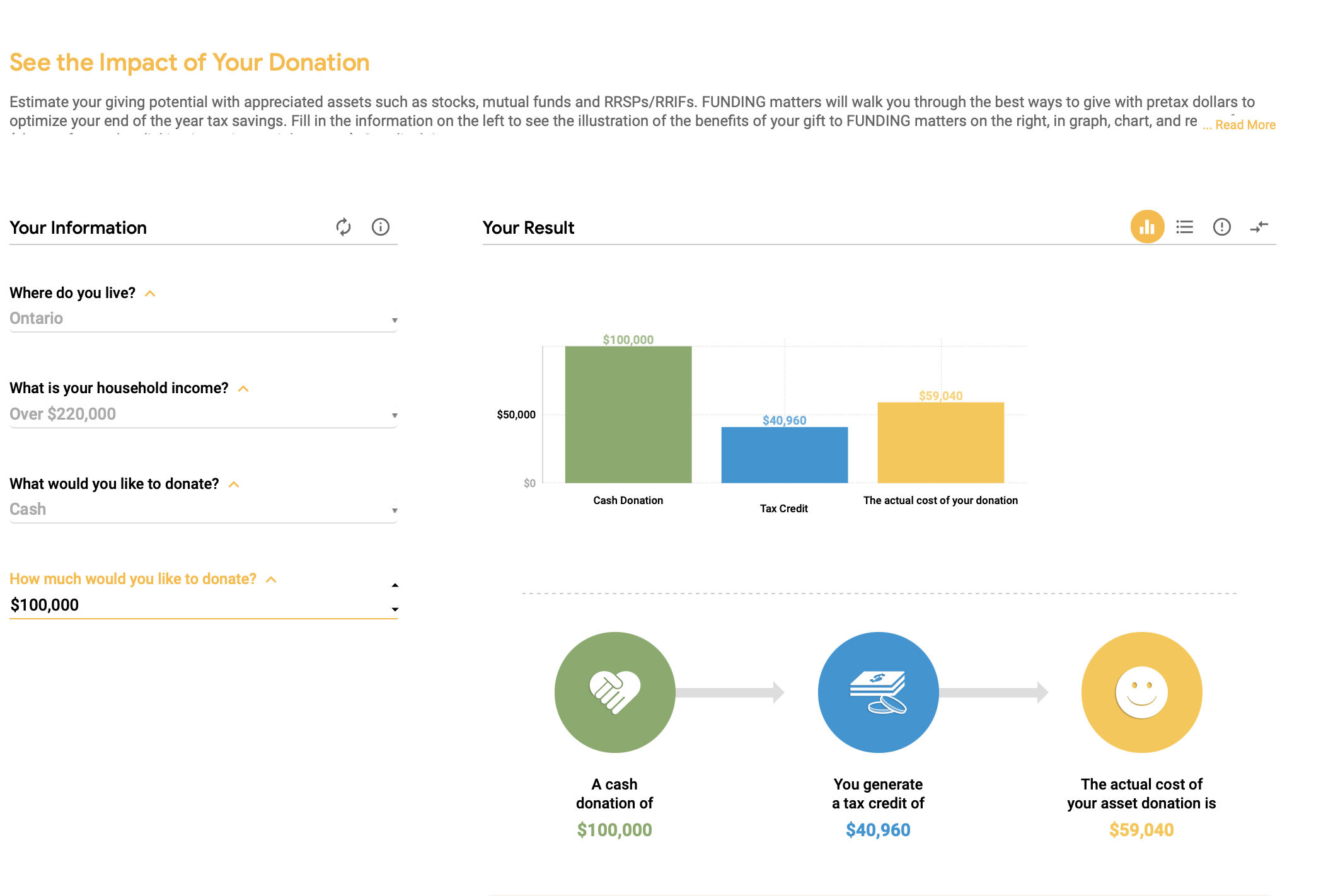

Online calculators aside, here’s an example to demonstrate the difference between in-kind gifting of $50,000 in shares, and selling the investment and then donating the cash.

If the gain in value on the investment is $40,000 (the adjusted cost base $10,000) in a non-registered account, half ($20,000) of that increase in value would be taxable if selling the shares and donating the proceeds.

For the highest income earner in Manitoba, the taxes would be a little more than $10,000, and the gift a little less than $40,000.

But if donated in-kind, no capital gains tax applies, and total gift would be $50,000.

Plus, donors get a non-refundable tax receipt worth about $23,000 to more than $25,0000 in tax savings, depending on their taxable income.

While more common among Canadians with significant wealth, folks of more modest means may have assets to give too, including ecologically sensitive land for a nature conservation group to protect. Others may have stocks in a non-registered account through workplace purchase plans or whatever the reason, not needed for retirement, to gift in-kind.

Plotnicoff notes the United Way receives in-kind gifts from all kinds of donors, ranging from a few hundred to tens of thousands of dollars.

Amanda Leuschen, vice-president of strategic partnerships and philanthropy at United Way Winnipeg.

Individual can choose to give from registered accounts too — though there is no benefit to doing so in-kind. All those accounts are tax sheltered, and when withdrawn from an RRSP, for example, the sum is fully taxable with applicable withholding tax (though you can make an election with CRA to not have that withheld). Assets inside TFSAs grow tax-free, so no taxes would apply anyway.

Still, you do get the tax credit for the amount donated for either account.

If you’re considering a donation, particularly an in-kind one, it’s best get on it as soon as possible because the assets must be in the charity’s account by Dec. 31 to be claimed for the 2021 tax year — and it can take a few days to complete, Plotnicoff says.

“If you’re planning to donate shares, don’t decide to do that on Dec. 30 because you won’t get it done in time.”

Fortunately, most charities, United Way included, are happy to guide givers through the process, Leuschen says.

“It’s just a neat way for people to be more empowered,” she adds. “People want to support the community and this is just another option that may suit them best.”